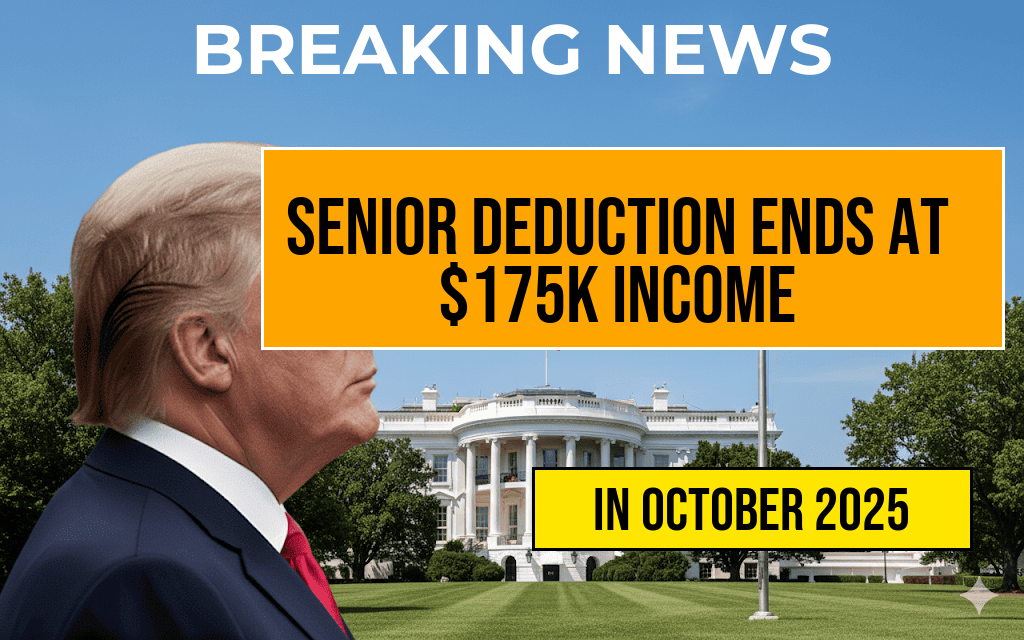

Taxpayers relying on the senior deduction are facing a significant change as the phase-out threshold has been revised. Starting this tax year, the deduction begins to gradually disappear once individual filers reach an income of $175,000. Previously, many seniors could claim a full deduction up to higher income levels, but the new policy narrows this benefit, potentially impacting thousands of retirees and senior households. This adjustment comes amid ongoing discussions about tax fairness and government revenue, prompting many to evaluate their financial planning strategies. The change aims to balance the federal budget while maintaining targeted support for seniors with moderate incomes, but critics argue it may disproportionately affect those on fixed incomes who see their deductions reduced as their earnings rise.

Understanding the Senior Deduction and Its Phase-Out

What Is the Senior Deduction?

The senior deduction is a tax benefit designed to provide additional relief to taxpayers aged 65 and older. It allows eligible seniors to claim a specified deduction amount, reducing taxable income and lowering overall tax liability. This provision has historically served as a financial buffer for retirees, many of whom rely on fixed incomes from Social Security, pensions, or retirement savings.

Recent Changes to the Threshold

Effective for the current tax season, the phase-out of the senior deduction begins once adjusted gross income (AGI) exceeds $175,000. The deduction gradually decreases as income rises, completely phasing out at higher income levels. Previously, the threshold for phase-out was set at a higher level, allowing many seniors to benefit from the full deduction well into their retirement years. The new threshold aims to target the benefit more specifically, aligning with broader tax reform efforts.

Details of the Phase-Out Schedule

| Income Range | Deduction Status |

|---|---|

| Up to $175,000 | Full deduction available |

| $175,000 – $185,000 | Deduction gradually decreases |

| Above $185,000 | No deduction available |

The phase-out process is designed to taper the benefit smoothly, reducing the deduction proportionally as income surpasses the threshold. Taxpayers with income just above $175,000 will see a partial reduction, while those earning above $185,000 will be ineligible for the deduction entirely.

Implications for Senior Taxpayers

Impact on Retirement Planning

Many seniors rely on deductions like this to offset their tax burdens, especially given their often fixed incomes. The reduction or elimination of the senior deduction at higher income levels could lead to increased tax liabilities for some households, prompting a reevaluation of retirement strategies. Financial advisors recommend seniors consider tax-efficient withdrawal plans and investment options to mitigate the impact of the phase-out.

Potential for Increased Tax Burden

While the policy aims to enhance fiscal responsibility, critics argue that it could place additional financial strain on seniors who previously depended on this deduction. For example, a senior with a $180,000 income might see their deduction reduced by nearly 50%, translating into hundreds of extra dollars owed at tax time. Such changes may influence decisions about work, investments, or estate planning, especially for those nearing the phase-out income level.

Broader Context and Reactions

Policy Rationale

Proponents of the adjustment emphasize the need to ensure that tax benefits are targeted toward those with moderate incomes, reducing loopholes and promoting fairness. The change aligns with efforts to streamline the tax code and generate revenue to support various federal priorities, including healthcare and social programs.

Criticism and Concerns

- Advocates for seniors warn that the phase-out could unfairly penalize those who have limited earning capacity but are still above the threshold.

- Some argue the policy does not sufficiently account for regional cost-of-living differences, which can significantly affect seniors’ financial situations.

- There is concern that the reduction may discourage savings or prompt early retirement among certain demographics.

Resources and Further Reading

Frequently Asked Questions

What is the Senior Deduction amount for taxes?

The Senior Deduction allows eligible seniors to claim up to Four Thousand Dollars in deductions on their taxable income.

At what income level does the Senior Deduction start to phase out?

The Senior Deduction begins to phase out once a taxpayer’s income reaches One Hundred Seventy-Five Thousand Dollars.

How does the phase-out of the Senior Deduction work?

As income increases beyond One Hundred Seventy-Five Thousand Dollars, the Senior Deduction gradually reduces until it is fully eliminated at higher income levels.

Who qualifies for the Senior Deduction?

Taxpayers must be eligible seniors, typically based on age and filing status, to qualify for the Senior Deduction.

Are there any strategies to maximize the Senior Deduction before it phases out?

Yes, eligible taxpayers can consider timing income and deductions or making strategic financial decisions to maximize their Senior Deduction before the phase-out begins at higher income levels.